Jeff Clark | Jan 7th 2019, 5:00:16 pm

While a myriad of forces pushed the gold price around in 2018, it basically ended the year flat. This report recaps the year in gold, shows how it compared to other asset classes in both short and long timeframes, and explores the factors to watch in 2019.

While a myriad of forces pushed the gold price around in 2018, it basically ended the year flat. This report recaps the year in gold, shows how it compared to other asset classes in both short and long timeframes, and explores the factors to watch in 2019.

The gold price traded in a fairly tight range in the first quarter of 2018, mostly between $1,300 and $1,350. Then it began to decline sharply in the second quarter, largely due to higher equity prices and strong GDP figures. It fell particularly hard from April through August (a seasonally weak period for the yellow metal), declining 15% from $1,365 to an 18-month low of $1,160.

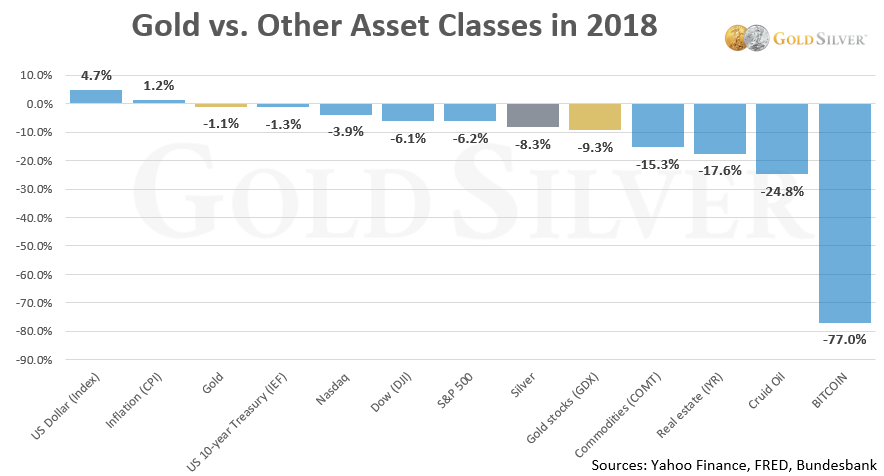

Once volatility returned to equity markets and global growth worries emerged, gold gained 10% from August to year end. December saw a 5% rise, gold’s strongest month since January 2017. It ended the year down 1.1%, its first annual decline since 2015.

As can be seen, the only asset class that rose last year was the US Dollar (and inflation). Gold was not the only investment that ended the year in negative territory, actually holding up better than most.

A strong US dollar, typically a headwind for gold, gained 4.7% in 2018. The US/China trade conflict pushed the US currency higher, along with the steady rise in interest rates.

Despite the tug of war in the gold market, volatility measures of the metal were near 10-year lows in 2018, only slightly higher than in 2017.

Meanwhile, gold remained one of the most liquid asset classes in 2018.

This high liquidity continues to provide a high degree of functionality to investors.

With 2018 in the record books, let’s widen the picture to examine gold’s long-term performance.

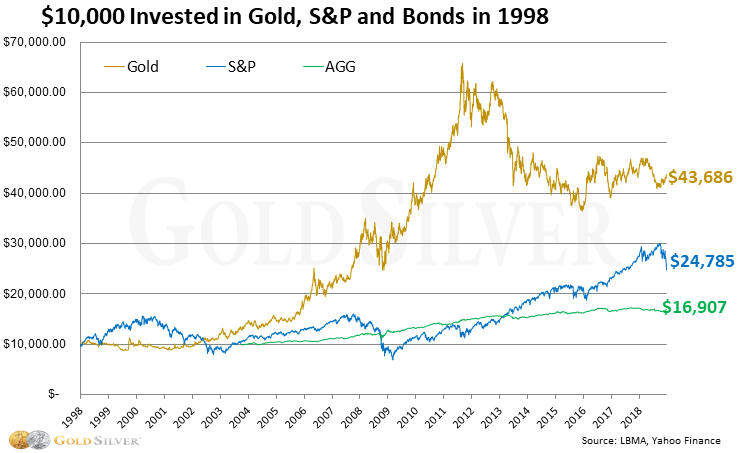

Over the past two decades, gold has experienced both bull and bear markets. Here’s how its performance compares to stocks and bonds since the champagne was popped back on New Year’s Eve 1997.

This has practical considerations. A simple $10,000 buy-and-hold investment in gold in 1998 has yielded a greater return than stock and bond investments.

Of course, gold’s greatest strength as an investment is most prominent when it is combined with these assets, since it tends to be inversely correlated, especially with the equity markets.

Given that context, what could be ahead for gold this year?

There are a number of factors and events that could potentially influence the gold market in 2019. Here are some of the most likely.

US Dollar: Depreciation Ahead?

A number of analysts have called for the US dollar to depreciate in 2018.

A weaker US dollar is a favorable condition for gold. When you add the possibilities of a slowing economy, falling oil prices, a stabilizing yuan, and tighter liquidity in U.S. markets, a weaker US dollar seems more likely than a stronger one in 2019.

Interest Rates: Will Hikes Slow or Even Stop?

Long-term bonds appear to be signaling that the Fed is likely done raising short-term rates. As further evidence, CME Group’s FedWatch Tool showed the first week of January that there was an 87% probability the rate would either stay at the current level or be lower by the end of 2019. Bets the rate would rise over the next 12 months have dropped to just 12%.

If US rate raises stop or reverse, gold would be more attractive, especially if real rates remain flat or negative. Globally, the amount of negative-yielding debt climbed over 46% in Q4 2018.

The flattening of the yield curve is also something to watch, particularly if it inverts, since this is frequently viewed as a sign of impending recession. Gold is typically sought as a safe haven during periods of negative economic growth.

Stock Market: Risk Is Greater to the Downside

After a 9-year non-stop run, it wouldn’t be surprising for stocks to take a breather, if not tip into a full-blown bear market. As former Fed chairman Alan Greenspan said recently, “It would be very surprising to see the stock market stabilize here and then take off.” Markets could still rise, he said, but the ensuing correction would be painful: “At the end of that run, run for cover.”

Strong words, but if his diagnosis turns out to be correct, the Fibonacci retracements based on the recent high in the S&P suggest lower stock prices are ahead.

Has a bear market already started? According to Hedge Fund Research, hedge funds collectively lost over 7% in 2018, the industry’s worst year since 2011.

At a minimum, volatility in the financial markets seems likely to continue. Falling stock prices and market turbulence have historically pushed increasing numbers of investors into the safe haven asset of gold.

Debt: Not Slowing Down

While debt is always with us, the concern at this juncture is that debt creation is no longer fostering a significant amount of economic growth. Virtually every category of society is weighted down with unsustainable debt loads:

US Federal debt: In just 10 years, it has grown from about 60% of GDP to 104%.

Consumer debt: Credit cards, auto loans and student loans (excluding mortgages) just hit $4 trillion. This is an all-time high, and was $3 trillion just five years ago.

Student loans: Total student loan debt is now $1.6 trillion, an all-time high. Of particular concern is that this amount is now larger than the amount of junk mortgages in late 2007 (about $1 trillion). Further, default rates on student loans are already higher than mortgage default rates were in 2007.

Corporate bonds: Over the last decade, the amount of corporate bonds outstanding has almost doubled, hitting $9 trillion. And nearly $2.5 trillion of that figure is rated BBB, nearly triple the amount of 2008. This includes stalwarts such as G.E., AT&T, Campbell Soup, Bayer, CVS Health, Sherwin-Williams, IBM, and Keurig Dr. Pepper. The particular concern here is that it can be more difficult to manage or bail out corporate debt than sovereign debt.

Leveraged loan market: Collateralized debt obligations, or CDOs, were valued at $61 trillion globally in 2007, according to the Bank for International Settlements. Despite attempts to regulate this sector and avoid or limit the damage caused by these instruments in the financial crisis of 2008, the total leveraged loan market has since doubled, based on the S&P/LSTA Leveraged Loan Index. S&P Global stated that "risks attributable from this debt binge are significant.”

China: China had about $2 trillion total debt in 2000. Today, it’s about $40 trillion, an increase of 2,000% in less than 20 years.

The levels of debt reached in many areas of society are not realistically repayable, except in radically inflated currencies. Either way, any fallout from a debt event or crisis, or a return to QE efforts, would draw investors to gold.

There are also factors within the gold market itself that bare watching.

Mine depletion, geopolitical risks, start-up delays, and a lack of industry investment over the past several years all point to lower gold production levels going forward.

Pinched supplies of new gold stocks could impact the price.

There’s a related concern for the mining industry: due to falling ore grades, production costs will likely never return to where they were a decade ago. Production costs ultimately serve as a floor for gold prices.

Despite some gold sales from Venezuela and Turkey in 2018 to offset currency declines (one reason why gold is so valuable), central banks have been net buyers since 2008.

While central banks in North America and Western Europe are not adding to their gold reserves, strong demand continues to be seen from Asia, Russia, Eastern Europe, the Middle East, South America, and Africa.

While retail demand for bullion hit an 11-year low in 2018, global fund holdings (including e-funds and depositories) remained buoyant.

Investment is the biggest variable among all demand sources. According to a Legg Mason survey of over 16,000 investors globally, a growing percentage cited gold as the best investment opportunity over the next 12 months. Roughly a quarter of those polled in Germany, Italy, Switzerland and the UK identified gold as the best investment opportunity. In the UK gold was seen as better than equities, bonds, cash, and alternatives.

As investment goes, so does the price.

View the oringinal article here: https://goldsilver.com/blog/2018-gold-snapshot-and-what-it-hints-about-2019/

GOLD: Here’s What’s Happening Right Now | May 23, 2023

Gold in Q1: Hello, Banking Crisis | Apr 19, 2023

Gold in 2022: A Year of Tumult, But Most Precious Metals Were Buoyant | Jan 25, 2023